The dollar traded higher versus majors yesterday after another move lower in the JPY, now trading at 6-week lows 108.00 versus the dollar and investor expectations for more ECB easing following today’s meetings. The dollar was also busted by US President Trump positive attitude towards the China trade talks, suspending tariffs on $250 billions by two weeks in October. The risk sensitive currencies like the AUD and YUAN were also being supported by the dovish US China trade talks. Global equity markets traded higher across the board led by the technology sector, sending all global markets higher in the US and EU equity markets. Metals traded near the flat line, caped by the stronger dollar and supported by US President Trump tweet for his desire to achieve negative interest rates in the US. Gold prices closed at $1,550 per ounce yesterday. Oil traded sharply lower following the ease in the US Iran sanctions, losing more than 2.5% and closing at $55.92 per barrel, yet being supported by the lowest US crude inventories in nearly a year, at 2% below their 5-year average for September.

The ECB Press Conference and Rate decision at 12:45 pm and US CPI at 1:30 pm are the important news on the agenda Thursday. (all times GMT).

| Global Markets 24 hours wrap-up | ||||||

|---|---|---|---|---|---|---|

| Market | GBPUSD | USDJPY | EURJPY | EURUSD | GOLD | OIL |

| 11.9.19 | -0.11% | 0.23% | -0.12% | -0.34% | 0.46% | -2.65% |

| USDMXN | USDCHF | AUDUSD | AUDJPY | USDCAD | Silver | Nat Gas |

| 0.18% | 0.1% | 0.01% | 0.26% | 0.34% | 0.16% | -1.16% |

| Dollar Index | DAX | FTSE100 | CAC40 | EURSXX50 | NIKKEI225 | CSI300 |

| 0.32% | 0.74% | 0.96% | 0.44% | 0.51% | 0.88% | 0.61% |

| 1 YEAR | 2.72% | 0.34% | 5.36% | 5.72% | -3.61% | 23.48% |

| Swing report | ||||||

|---|---|---|---|---|---|---|

| TRADE | ENTRY PRICE | POSITION | OPEN PROFIT | DATE TRIGGERED | STOP LOSS | UPDATES |

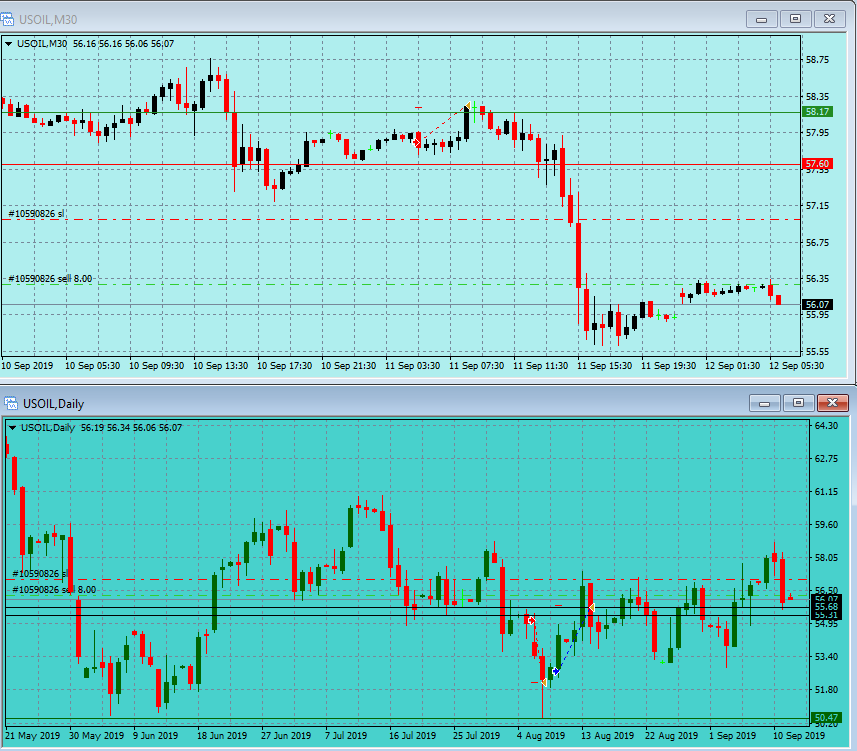

| OIL | 56.28 | 8 | 150 | 12/9 | 57 | new position |

| OIL | 57.84 | 8 | -328 | 11/9 | 58.25 | stopped out |

| GOLD | 1490 | 60 | 340 | 9/9 | 1480 | |

| OPEN PROFIT | $490 | |||||

Gold long trade looking for the $1,550 level, looks stronger this morning.

OIL trade missed the 2.5% move lower yesterday by 6 cents, “bear flag” short entry posted this morning, looking for more downside in oil on the US Iran tensions ease.

Warning: The information provided on this page (“the information”) is for instructional purposes only, for enhancing your general knowledge of the capital market in general and using trading methods and the technical analysis method in particular. We hereby clarify that the company, its management, staff, shareholders and agents do not hold investment advisor licenses and/or portfolio manager licenses by any applicable law, and do not pretend to advise any person on the worthiness of buying, selling, holding or investing in securities and other financial assets. The information should not be construed to be a recommendation or opinion, and any person who makes any decision based on the information – does so entirely at their own risk. Be aware that the information cannot serve in lieu of advice which accounts for specific information and needs of an individual, and that investing in securities and financial assets may cause loss. The company, its management, staff and agents may have a personal interest in issues related to the information, and may hold specific securities mentioned in the information, or similar securities. If you use the information, you waive any claim or demand against the company or anyone acting on its behalf.